The White House released its FY2027 budget this morning. It is 92 pages long. The most important number is on page 139. The federal government paid $970 billion in interest last year.

This year it crosses $1 trillion.

That is not a projection. It is already happening. In 2026 the Treasury is rolling $9.6 trillion in debt borrowed near zero percent interest into today’s market at 4.3 percent — same debt, dramatically higher payments. Nobody voted for that increase. Nobody announced it. It compounded quietly while everything else was happening.

In this article we are going to filter out the fluff, find the facts, and take a look at planned economic events between now and the fall elections.

In 1869, John Wesley Powell launched into the Colorado River at Lee’s Ferry in a wooden boat. He knew his starting elevation. He knew where the river ended. He did not know what the canyon looked like in between. Powell was genuinely afraid there was a Niagara Falls somewhere in the middle. Let’s get in our raft and check out the rough water ahead.

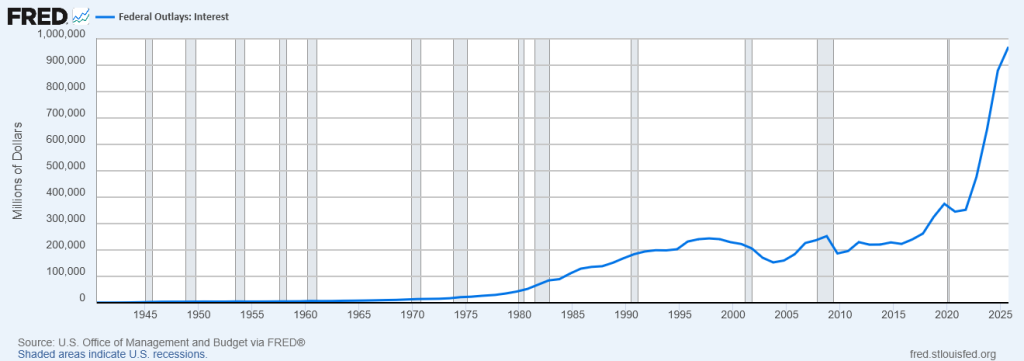

The Chart That Tells the Truth

Source: U.S. Office of Management and Budget via FRED®, Federal Reserve Bank of St. Louis

Look at that line.

From 1940 to 2020 — eighty years — interest payments grew slowly from near zero to $345 billion. A long, gradual curve. Manageable at every step.

Then look at what happens after 2020.

$345 billion in 2020. $475 billion in 2022. $660 billion in 2023. $882 billion in 2024. $970 billion in 2025. The line goes nearly vertical. No recession caused it. No emergency triggered it. The debt existed before. The interest rate changed. That was enough.

The White House projects this line flattens out. Rates fall, they say. Growth accelerates. The curve bends back down. Here is why that is not what the data says.

What the Budget Actually Says

The FY2027 budget contains three summary tables. They show discretionary spending by agency. They show economic assumptions. They do not show total revenues, total outlays, or the deficit. Those numbers are in a separate companion document.

That is worth pausing on. The headline budget document does not show the deficit.

The companion document does. Here is what it says for 2027: total revenue $5.9 trillion, total spending $7.9 trillion, deficit $2.0 trillion, net interest $1.1 trillion.

The Department of War — formally renamed from Defense — receives $1.45 trillion. Up 43.7 percent from last year. Non-defense programs are cut 10 percent across the board.

Those are the official numbers. Now here is what they assume.

Three Assumptions That Don’t Hold

Interest rates fall. The White House projects 10-year Treasury rates declining from today’s 4.3 percent to 3.5 percent within two years. Rates were 4.0 percent last November. They are 4.3 percent today. The direction is up, not down. The budget assumes a trend that is running in reverse.

Tariff revenue nearly doubles. Customs revenue is projected to jump from $195 billion last year to $464 billion in 2026. That $270 billion increase funds most of the revenue growth story. It rests on a contradiction. Tariffs designed to end foreign imports cannot simultaneously be a reliable revenue source. When trade adapts — and it always does, permanently — that revenue disappears and does not come back.

GDP grows at 3.1 percent. Moody’s Analytics puts the probability of recession within 12 months at 49 percent. The White House projects 3.1 percent real growth. One of these is serious analysis.

Remove these three assumptions. Replace them with today’s actual numbers. Revenue drops from $5.9 trillion to approximately $5.4 trillion. Interest costs rise from $1.1 trillion to $1.7 trillion by 2027 as the $9.6 trillion rollover completes at real rates. The deficit does not improve. It widens.

The Shadow Budget

There is a gap between what the budget document shows and what is actually being spent. It is large and it is documented.

The companion document shows baseline defense spending of $953 billion for 2027. The policy budget requests $1.45 trillion. That $500 billion gap does not appear in the headline deficit number. Baseline projections assume current law. The war is not current law. It is an ongoing emergency funded through supplemental requests that bypass normal appropriations.

The $200 billion emergency war supplemental requested this month does not appear in these tables. Neither does the $1.5 trillion October request. Congress is split 50/50 and cannot pass either one. The spending continues anyway through executive authority. The bills accrue.

This is the shadow budget. Not a conspiracy. A structural feature of how emergency spending works. The gambling addict does not announce the cash advance. It appears later, when the reckoning arrives.

Where the River Goes

Here is the interest payment trajectory when you use real rates instead of hoped-for ones.

| Year | Interest Paid | Federal Revenue | Interest as % of Revenue |

|---|---|---|---|

| 2020 | $345B | $3.4T | 10% |

| 2023 | $660B | $4.4T | 15% |

| 2025 | $970B | $5.2T | 18.5% |

| 2027 (real rates) | $1.7T | $5.4T | 31% |

| 2029 (real rates) | $2.9T | $5.5T | 53% |

At 53 cents of every revenue dollar consumed by interest alone, the discretionary government does not exist in any meaningful sense. Social Security, Medicare, Defense, and interest together exceed total revenue. Every other function of government — courts, border, education, infrastructure, research, diplomacy — is borrowed before it is spent.

This is not a prediction. It is arithmetic. The starting numbers are confirmed. The direction is locked. The pace is the variable.

Our earlier article — The Perfect Economic Tsunami of 2026 — describes the eight forces driving that pace. Private credit collapse. War spending with no exit. Congressional paralysis. Foreign capital withdrawal. Each one is a rapid in the canyon. Together they determine whether the descent is fast or catastrophic.

The Three Tools at the Bottom

There are exactly three ways out of a budget that cannot be balanced. Every policy proposal from every future administration is a version of one of these.

Default. Stop paying. Argentina did it in 2001. Their middle class was wiped out in months. The global financial system has no contingency plan for a US default. Reserve currency status ends the same day.

Inflation. No vote required. No announcement. The real value of the debt shrinks while the nominal number stays the same. The working class pays through eroding wages and savings. The asset-holding class is partially protected. This is the tool that requires no courage and leaves no fingerprints. It will be the first one reached for.

Restructuring. Formal renegotiation with creditors. The only tool that addresses the structural problem. Requires cooperation from China, Japan, and Saudi Arabia at the exact moment America has burned every diplomatic relationship it had. The last option considered. Probably the one that eventually happens.

Choose Your Boat

Powell’s wooden boats sit calm in that photograph. The canyon walls rise around them. The water looks still. Three members of his expedition eventually climbed out over the rim. They could not take the uncertainty. They were never heard from again.

Powell stayed in the boat. His boats were battered. He lost supplies at every major rapid. He portaged around the ones he could not run. He made it through.

The rigid boat — fixed income, fixed expenses, cash savings, a career in a sector that cannot flex — absorbs every rapid as a direct hit. The rubber raft bounces off the rocks and keeps moving. It looks chaotic in the white water. It exits downstream.

The canyon is real. The river is moving. The question is not whether you go through it. The question is what you are sitting in when you do.